As temperatures climb across the country, Canadian car buyers may find some relief—not just from the weather, but from improving credit conditions that could make auto financing more accessible. The latest data from Cox Automotive’s Dealertrack Credit Availability Index shows a positive shift in auto credit trends, with implications that extend beyond the U.S. and into the Canadian market.

Credit Conditions Improve for a Second Straight Month

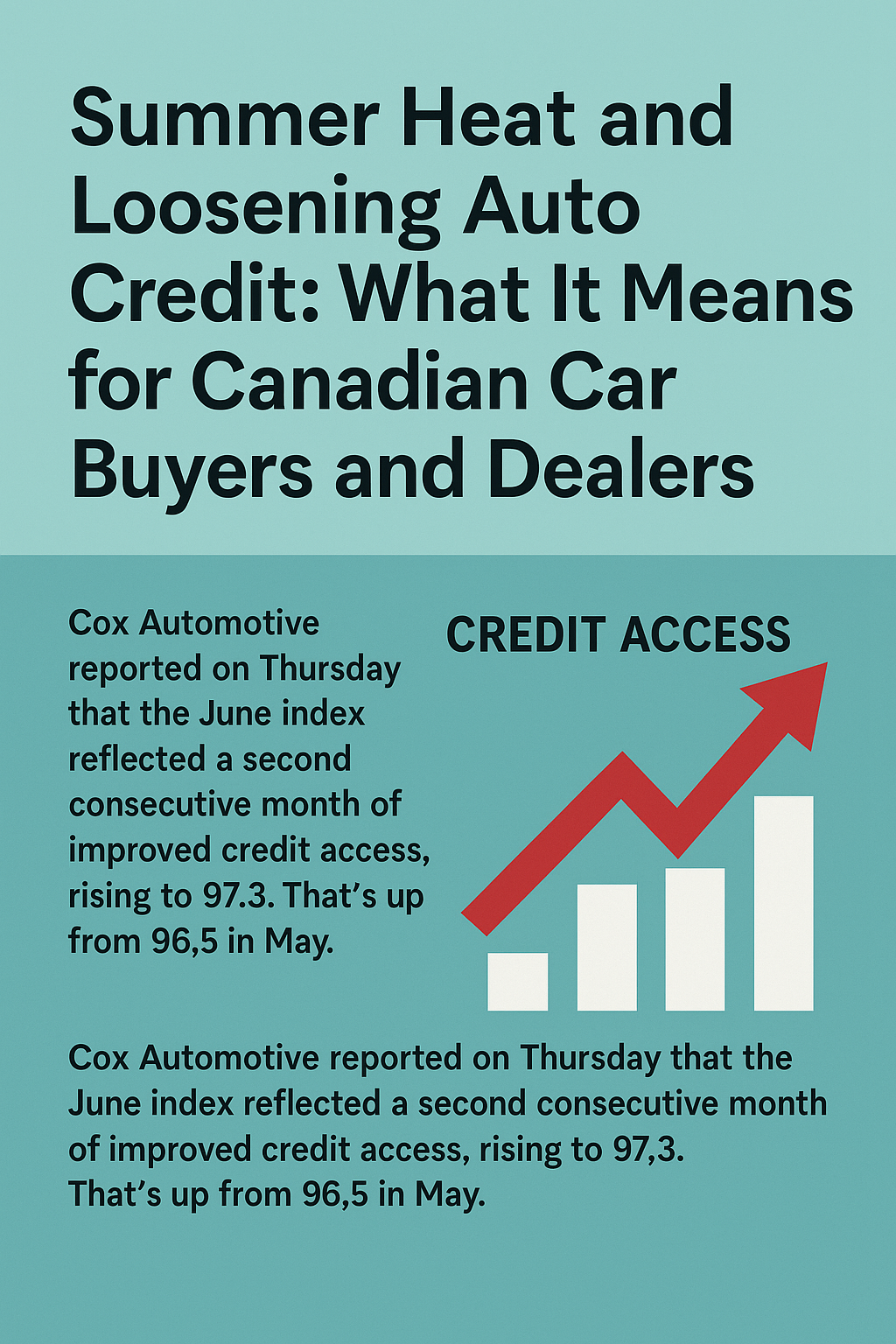

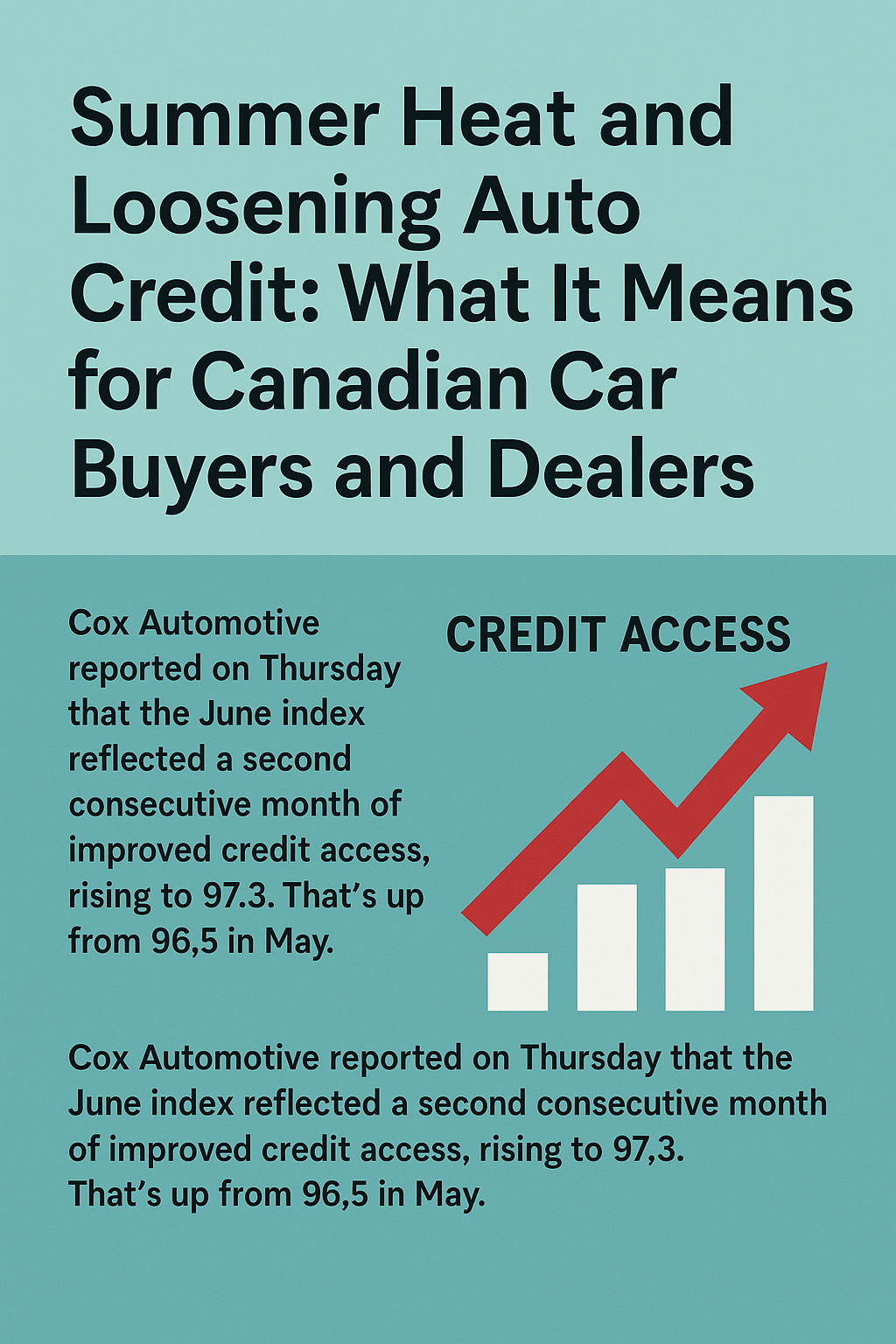

In June, the Dealertrack Credit Availability Index rose to 97.3, marking a second consecutive month of improving access to auto loans. That’s up from 96.5 in May and represents a continuation of a broader loosening trend that began in late summer 2024. While the index is U.S.-focused, its trends are relevant for Canadian dealers and lenders keeping a close eye on North American credit conditions.

The brief hiccup in April—attributed to market uncertainty following tariff-related policy shifts—has given way to a rebound, and credit is becoming more available again across multiple lending segments.

What This Means for the Canadian Market

Canadian consumers and dealers may not see a one-to-one reflection of U.S. credit trends, but the underlying dynamics are often aligned. Lower borrowing costs, increased lender participation, and competitive rate structures typically flow across borders, especially given the interconnected nature of North American automotive finance.

If Canadian lenders are following the same trajectory, we can expect:

- More approvals, even for borrowers with mid-range credit.

- Expanded subprime lending, giving a second chance to higher-risk applicants.

- Slight drops in borrowing rates, offering potential monthly savings.

These changes could be particularly meaningful for used vehicle buyers and small-town dealers in Canada, where affordability and flexible financing options are critical to moving inventory.

The Six Key Credit Factors to Watch

The Dealertrack Index tracks six metrics to assess overall credit access. Here’s how they’re trending and what that might signal for Canadians:

- Approval Rates: Up 70 basis points in June, suggesting lenders are more comfortable extending credit—likely due to more stable borrower profiles and competition.

- Subprime Share: Increased by 10 basis points. In Canada, this might translate into more financing opportunities for newcomers, younger buyers, and those recovering from financial hardship.

- Yield Spread: Largely flat, reflecting disciplined lender pricing. This is important for Canadian lenders balancing rate competitiveness with profitability.

- Term Length: Loans over 72 months increased by 80 basis points, continuing a trend toward longer-term financing. For Canadian buyers, this often means more manageable monthly payments, though at the cost of higher total interest.

- Negative Equity: Steady at 54.8%—still historically high. With Canadian trade-in values stabilizing, negative equity remains a concern, especially for those rolling balances into new loans.

- Down Payments: Dropped by 40 basis points. This could reflect stronger competition or greater lender flexibility, but Canadian consumers should be wary of undercapitalized loans.

Lenders Are Not All Alike

The loosening of credit access was most pronounced among finance companies and captive lenders, who tend to be more aggressive in growing their loan portfolios. In contrast, banks and credit unions—including Canadian institutions like RBC, TD Auto Finance, and Desjardins—were more cautious.

This divergence highlights the importance for Canadian buyers to shop around—some lenders are clearly more willing to negotiate and take on moderate risk to gain market share.

Final Thoughts: Opportunity for Dealers—and How Our SAM Widget Helps

The continued improvement in credit access opens up a timely opportunity for Canadian dealers to close more deals and serve a broader range of customers. But identifying the right financing opportunity quickly and accurately remains a challenge, especially with shifting lender appetites, longer terms, and varied approval criteria.

That’s where our F&I Credit Decisioning Widget (Called SAM) steps in.

Whether embedded on your dealership website or used by your sales team in-store, our widget dynamically matches each customer to the lender most likely to approve their profile—in real time. Here’s how it can help:

- ✅ Boost Conversion Rates: Instantly align customers with lenders that fit their credit profile, even as credit conditions change.

- 🔍 Surface Subprime Opportunities: As subprime credit access expands, our widget helps uncover deals that might otherwise be overlooked or declined.

- 🧠 Streamline F&I Workflow: Our system factors in loan term preferences, down payment flexibility, and rate fluctuations—reducing the back-and-forth and speeding up approvals.

- 📈 Support More Informed Sales: Sales advisors can confidently present finance options tailored to the buyer’s actual likelihood of approval, not just guesswork.

- 📊 Track Market Trends: Our backend analytics help dealers spot shifting approval trends by lender type, borrower profile, and vehicle category—so they can adjust sales strategies accordingly.

As more Canadians re-enter the vehicle market this summer, dealers who leverage smart credit-matching tools will be best positioned to thrive in this new lending landscape.