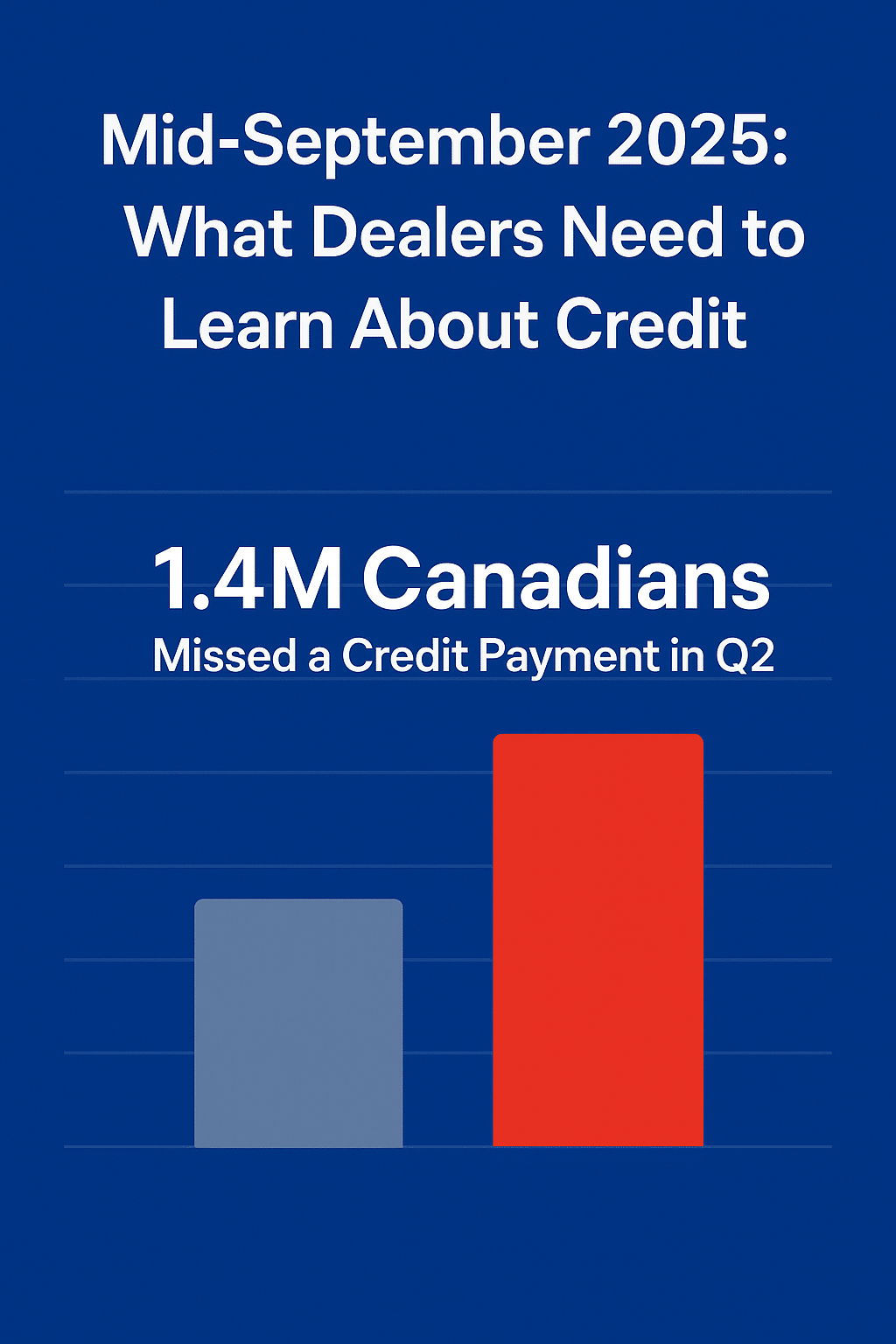

Auto finance is entering a more complex risk environment. According to TransUnion’s latest Consumer Credit Forecast, auto loan delinquencies are projected to rise for the fifth consecutive year, with accounts 60 days or more past due expected to reach approximately 1.54 percent in 2026.

While the increases remain incremental, the trend itself is unmistakable. Inflation continues to pressure household budgets, unemployment is expected to tick slightly higher, and consumers are managing more competing financial obligations than at any point in recent years. Together, these factors are reshaping how risk shows up across auto portfolios.

What the data is telling us

The TransUnion forecast highlights three important signals for lenders and dealers:

- Auto loan delinquencies are climbing steadily, even as growth moderates year over year

- Risk is not isolated to one product, with mortgages and unsecured personal loans also seeing upward pressure

- Macroeconomic uncertainty remains the dominant driver, meaning volatility, not collapse, is the most likely scenario

This is not a return to crisis conditions. Instead, it is a prolonged period where traditional assumptions about borrower behavior are less reliable.

Why traditional underwriting falls short

Many lenders still rely on static score cutoffs and backward-looking rules. In a rising-delinquency environment, this approach creates two costly outcomes:

- Good customers are declined unnecessarily, reducing volume

- Higher-risk customers slip through without early warning, increasing loss severity

When delinquencies rise slowly over several years, the margin for error shrinks. Precision matters.

How better decisioning changes the outcome

Modern decisioning platforms enable lenders to respond dynamically rather than defensively. By combining alternative data, real-time signals, and explainable models, lenders can:

- Detect early risk shifts before accounts become delinquent

- Adjust approval, pricing, and term strategies without blunt tightening

- Maintain growth while protecting portfolio performance

At DecisioningIT, we help organizations move beyond binary approve or decline decisions toward adaptive strategies that reflect how consumers actually behave in today’s economy.

The takeaway

Rising auto delinquencies are not a surprise. What will separate market leaders from the rest is how intelligently they respond. In an environment defined by gradual but persistent risk, smarter decisioning is no longer optional. It is a competitive advantage.

If you would like to explore how advanced decisioning can help you balance growth and risk in today’s auto market, we would be happy to talk.