Automotive dealers: what percentage of your customers are you leaving to used vehicle dealers who specialize in automotive financing?

Most dealerships simply don’t know the answer.

For nearly three years, I traveled across Canada meeting with executives from some of the country’s largest dealership groups.

I asked every one of them the same question:

What percentage of your customer base falls into the alternative credit segment?

The answer was almost always the same.

“Around 5%.”

But they weren’t talking about credit applications.

They were talking about completed sales in the alternative credit segment.

And those are two very different things.

As we dug deeper, I realized that very few dealerships had visibility into how many customers had applied with an alternative credit profile. That information simply wasn’t available to them.

In other words, they knew the final outcome… but not everything that happened before.

- The customer dismissed by the sales team because they were assumed to be unfinanceable.

- The newcomer who is immediately asked for a 25% down payment without first verifying the latest lender programs available.

- The customer who leaves convinced that financing simply isn’t an option.

None of these files ever appear in the dealership’s monthly reports.

You never see them.

Yet these are often the customers who end up purchasing from used vehicle dealers specializing in automotive financing.

“I had never looked at it that way… because I simply couldn’t measure that metric.” That was the response I heard over and over again.

Measuring only what gets sold tells only part of the story.

Measuring what enters your sales process—prequalification requests, leads, and in-store credit inquiries—reveals the opportunities that exist long before a sale is ever completed.

With a real-time dashboard and monthly reporting, dealerships can now monitor how many customers enter their financing pipeline, understand their credit profile, and compare that number with the deals that actually become sales.

The gap between the two is more than just a statistic. It represents opportunities that deserve a different approach—starting with credit prequalification.

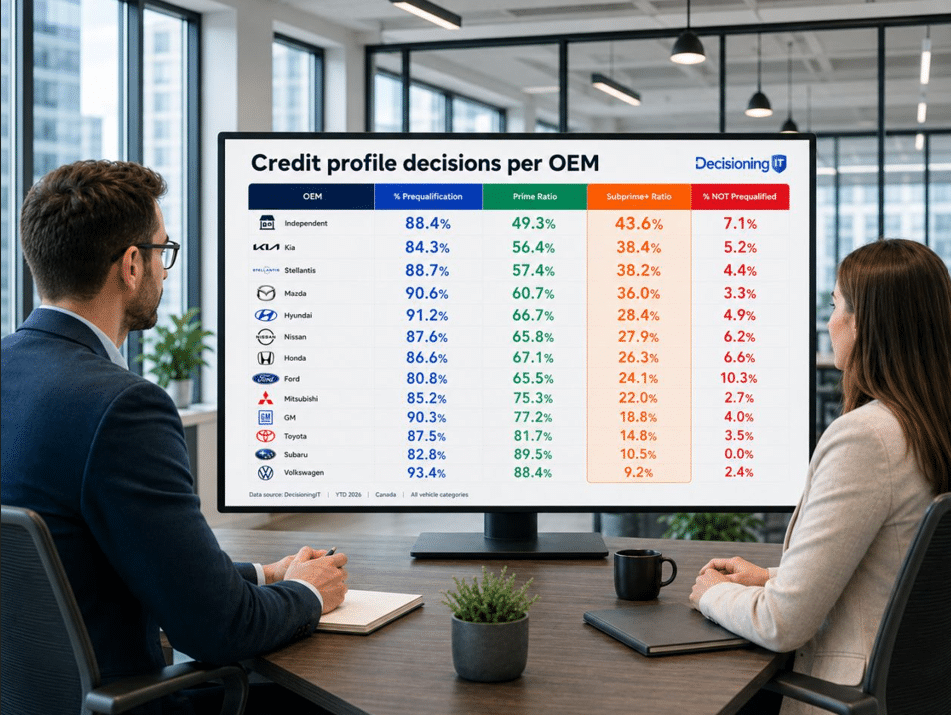

Before drawing any conclusions, take a look at the data below.

These are not sales figures.

They represent the real credit applications submitted by consumers.

Now compare those numbers with your own sales.

The gap often tells a much more interesting story than the sales results themselves.